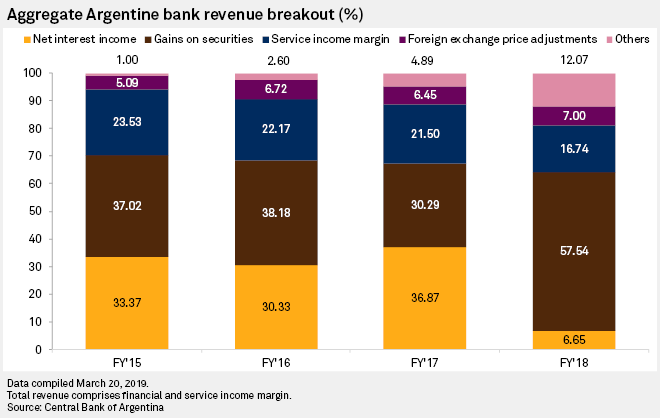

Less than a tenth of revenues generated by Argentine banks in 2018 came from lending activities, underscoring the dramatic shift financial institutions there have made to withstand ongoing economic volatility.

While banks in the country overall posted solid profit increases for the year — even after accounting for Argentina’s 47.6% inflationary spike — a larger proportion of the income supporting the growth came from securities. According to data collected by S&P Global Market Intelligence, 57.5% of banks’ total income came from financial securities in 2018, up from 35.2% averaged in the three years prior. The percentage of revenues from net interest income, meanwhile, sank to 6.7% from 36.9% a year earlier.

With loan growth not expected to pick up again until 2020 at earliest, the reversion to securities-dependent income — a strategy banks in the country had embraced for years prior to current President Mauricio Macri administration — is likely to continue.

“By definition, this (securities’) stream of revenue is non-recurrent and non-sustainable for banks, but the truth is it has proven to be,” Valeria Azconegui, a senior analyst at Moody’s, said.

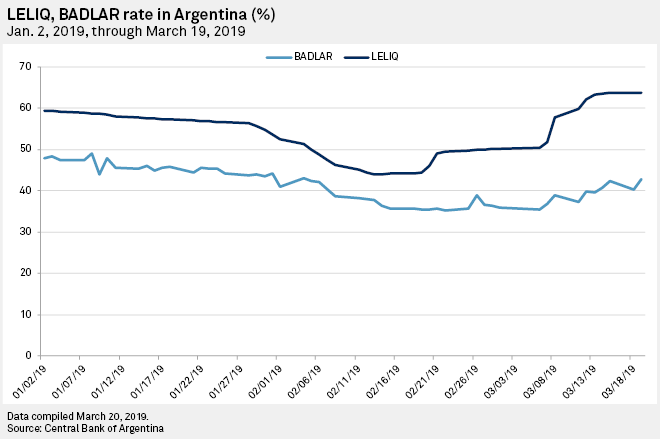

“The figures banks are pulling from Leliq (investments) are really good … (they) yield an incredible rate,” said Santiago Gallo, director of financial institutions at Fitch Ratings. “In the longer term, lending is a more sustainable business. [When it’s] not, banks turn into money desks.”

Along with underlying dollar pressures and rampant inflation, an especially high 65% interest rate on Banco Central de la República Argentina’ Leliq notes have again become the main obstacle for credit growth to resume, experts say. Borrowers have been discouraged from taking on new debt, as the annual interest rate on some loans are now at or above 100%. Banks meanwhile, are less willing to take on risk, given lingering economic and political uncertainty ahead of a presidential election later this year.

“There is a deep retraction in credit, both on supply and demand,” Daniel Marx, a former secretary of finance in Argentina, said in an interview. “Looking forward, I would not expect substantial trend changes in the upcoming months and even up to early next year,”

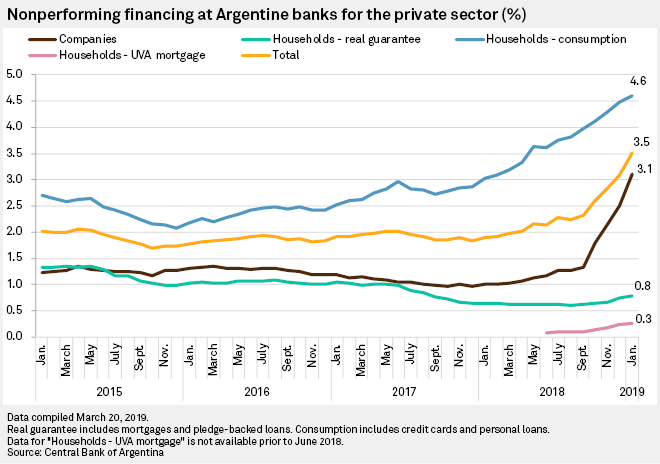

Central bank data from January shows local currency real credit to the private sector plummeted nearly 20.6% over the last 12 months, driven by private banks. Broad financing to companies fell 13.2% year over year.

“The (monetary) rate is so high that the bank might say, ‘truthfully, this risk no longer compensates me. What use could I make of charging a (high) rate on an SME or on a personal loan if I know that in two or three months I will be paying that with provisions?’ They choose to stay on standby, and invest in instruments like Leliqs,” Azconegui said.

The impact of the recession has also started to bleed into credit quality. Banks’ nonperforming loan ratio topped 3.5% in January, and Moody’s estimates it will climb to 4.5% by year-end.

“These levels are not worrisome since provisions cover them, but my impression is that (the portfolio) will continue to deteriorate. The trend does not end here,” Marx said.

Provisions at top banks surged in the last quarter of 2018, doubling to 2% of total assets from 1% previously, according to figures compiled by Quantum, a local consultancy firm.

Despite the expectation for deteriorating credit quality, banks have leveraged government securities to significantly bolster their results. In part, they have benefited from a widening spread between the Leliq rate, which has jumped by more than 20 percentage points in recent weeks, and the Badlar, the rate banks use to set the rate on fixed-term deposits, which has ticked up by just 7 percentage points.

In a recent earnings call, CFO of Banco Macro SA Jorge Scarinci stressed how that “spread (against time deposits) was extremely positive for the bank” in the fourth quarter.

Going forward, Fitch Ratings expects negative real growth in credit in 2019, while 2020 is still clouded in uncertainty. “Everything will be dictated by the electoral result, and even if Macri wins there is nothing guaranteed. He still has to improve his accuracy with the economic policy,” Gallo said.

As of March 22, US$1 was equivalent to 42.05 Argentine pesos.