Financial markets increasingly expect Brazil’s benchmark Selic interest rate to hit new record lows this year as economic growth forecasts for the country have become continuously less impressive.

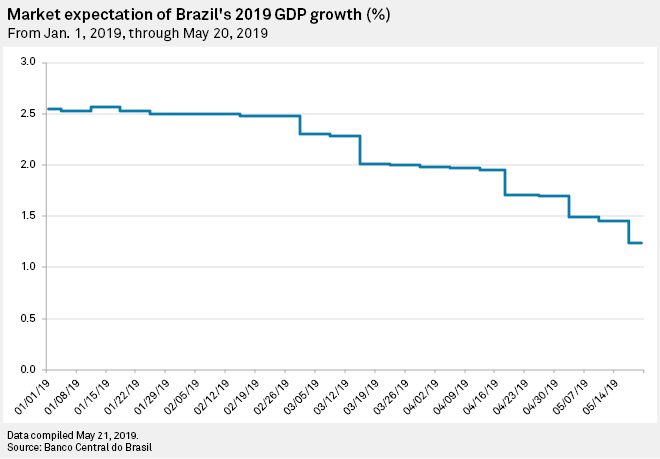

In the latest Banco Central do Brasil’s market survey, financial agents trimmed forecasts for economic growth for the 12th time in a row. It now sees growth for 2019 at just 1.24%, about half the rate it had expected when Brazilian President Jair Bolsonaro took office at the start of the year. The official government forecast is now at 1.60%, down from a prior estimate of 2.2%.

“The economy is truly not responding,” Renato Ometto, a partner with Mauá Capital, said in an interview. Ometto called the weak growth “frustrating,” noting the high expectations for Bolsonaro’s government. But he also believes that it is a “natural” occurrence as the new administration is still “getting educated” on the inner workings of Brazilian politics.

The continuous decline in economic growth expectations has been largely blamed on government delays in passing highly anticipated structural reforms. According to economists, the government’s focus on securing pension reform has put every other reform on hold, whether it be tax, privatizations or bureaucracy cleanups. That has led consumers and investors to sit on the sidelines, leading to GDP stagnation.

The Bovespa index has already receded 5.5% from a record high above 100,000 points hit in mid-March, while five-year credit default swaps for Brazilian debt have ticked 16.2% over that time.

“Pension reform is jamming the local market,” Canepa Asset CEO Alexandre Povoa wrote in a recent report, echoing a sentiment that Brazil’s central bank itself noted. “Uncertainties about fundamental aspects of the future economic environment — notably fiscal sustainability — have adverse effects on economic activity … in particular [on] investment decisions that involve a high degree of irreversibility,” the bank said in the minutes from its latest monetary policy meeting.

As result, GDP growth for the first quarter is expected to be next to zero, and the central bank has even admitted that there is a “relevant possibility” it contracted slightly.

Some investors believe that the sluggish growth gives authorities room to further reduce interest rates from an already record low 6.50%.

“A reduction of rates is a good scenario for the economy in terms of stimulating potential growth and [making] more credit available at a decent yield, which we have never seen before,” Ometto said.

Analysts at Bank of America Merrill Lynch went even farther, saying in a recent report that the “monetary policy impulse is weaker than expected and rates should be lower … even under pension reform approval.” The bank expects 100 basis points worth of rate cuts over the course of 2019 once Brazil’s lower chamber approves the reform bill. That would put see the Selic rate at 5.50% by year-end.

Such a reduction would mark a reversal from expectations earlier this year that envisioned the Selic rate would hold flat at 6.50% for the whole of 2019.

Lower rates a “game changer”

An extended period of time with an even lower Selic rate could be a “game changer” for Brazil, market experts said, as it would have a profound impact on the availability of credit and the behavior of local investors who no longer have easy double-digit returns.

“Our interest rates have been historically so high that anyone could leave money in the bank and get 10% to 12% per year. Because rates are so low now, people see monthly returns do not make up for expenses anymore and might be willing to take more risk,” Ometto said.

This could drive business opportunity for Brazilian asset managers. Carlos André, CEO of market leader BB Gestão de Recursos-Distribuidora de Títulos e Valores Mobiliários SA, recently told Valor Economico that the low rate environment already is driving a “change of mix in the investment industry.”

BB DTVM, which may pursue an IPO in the near future, expects to grow its roughly 1 trillion real whole portfolio by up to 12% this year. Its equity funds were the fastest growing type in the 12 months to March, up 18.3% year over year.

Industry figures pulled by ANBIMA association support a similar trend. In 2018, stock funds outpaced the rest of financial products with a 23.5% yearly growth to over 300 billion reais under management.

Volatility ahead

Though analysts remain mostly positive on Brazilian assets, high volatility is expected to continue in the coming months as the pension reform bill works its way through four voting rounds in Congress. The first round of voting is expected to start in August, and many hope that full ratification will come in September.

Most industry observers believe that the reform will pass, though they warn the ultimate version is likely to be a diluted form of what Bolsonaro’s economic team initially proposed, which targeted more than 1 trillion reais in savings.

The extent of that dilution is still unknown, though Ometto said legislation that creates anything less than 700 billion reais in savings will leave economic growth vulnerable.

As of May 22, US$1 was equivalent to 4.03 Brazilian reais.