Both traditional banks and financial technology firms have benefited from a surge in digital account openings during the COVID-19 pandemic, though questions remain on how some of these companies can monetize these new customers.

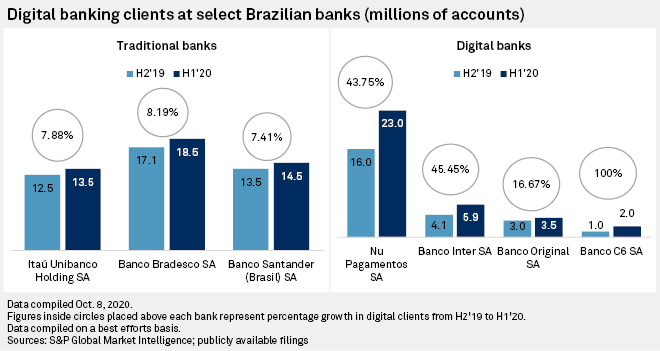

The country’s three largest private banks added 3.5 million digital clients in the first half of the year, averaging a roughly 7.7% growth rate. Many fintech players saw even stronger growth, ranging between 40% and 50% for the six-month period.

“Whether digital or traditional, every bank in Brazil benefitted from this trend,” Geraldo Rodrigues, a director with Banco Santander (Brasil) SA, said in an interview. “Though digital acquisition was a reality before the pandemic, truth is it acquired an accelerated pace after it.”

Santander Brasil’s digital sign-ups rose 7.4% in the first half to 14.5 million clients, and the company expects to add 2 million more by the end of the year — more than it had recorded in the prior three years combined.

“A lot of our energy has been put in digital conquest,” he said. “It as a great opportunity to bring in customers you did not reach before with the branch network.”

To be sure, mobility restrictions and social distancing measures have driven a greater number of individuals and businesses to seek alternatives to in-branch banking. It has also driven more unbanked or underbanked individuals — those who rely prominently on cash transacting — toward digital products. The distribution of pandemic-related government aid also helped.

“Almost half the population in Brazil is receiving this benefit” Maxnaun Gutierrez, head of products and individuals with Banco C6 SA, said in an interview. “This ushered the unbanked population to open accounts at banks and digital wallets in order to collect the money.”

But while traditional banks are making a greater effort, growth has widely favored digital-born players. Nu Pagamentos SA’s Nubank, Brazil’s largest digital bank, added 7 million new account holders in the first half of the year, double the number of the big three traditional banks combined. Smaller digital banks have seen similarly impressive growth.

“The largest banks’ mobile aspect was not prepared for this kind of avalanche,” of digital account sign-ups, said Antonio Bernardo, a senior partner at Roland Berger. “You might need to send four or five documents at a traditional bank [to open a digital account], while at a digital lender it takes roughly 5 or 10 minutes.”

Mobile phone data reflects that trend. The mobile apps for several fintech players — MercadoLibre Inc.’s Mercado Pago, Nubank, Serasa, Banco Original SA’s PicPay Serviços Ltda., PagSeguro Digital Ltd.’s PagBank and Banco Inter SA — ranked among the 10 most popular downloads on both Android iPhone devices at the end of September, according to Sensor Tower data. Apps for traditional banks like Banco Bradesco SA, Itaú Unibanco Holding SA, and Santander Brasil, ranked lower.

But despite their success in winning new clients, some experts note that digital players have yet to fully translate it into greater profits. Digital credit in itself is still only a fraction of total credit, and lenders strain to increase their offering in order to better cross-sell and drive further usage of services.

Digital banks “have not yet been able to activate their clients,” in a profitable way, Roland Berger’s Bernardo said. “They signed them up, opened accounts on the platform, but could not build on top of that … The number of clients is a fantastic thing to have, but if you lose money,” there’s not much benefit.

In order to compensate for a more limited product offering, digital banks have applied capital to expand into different niches as well and grow their ecosystem of services. Nubank recently acquired online broker Easyinvest, while Banco BTG moved into digital retail banking on top of its investment banking services.

“We need to have a lot of products” in order to compete with traditional banks, C6’s Gutierrez said. Clients that focus solely on the unbanked can do with fewer products, he explains, but if wanting to tap people already in the system or cross-sell more intensively then a wider array of products needs to be enhanced.