Banks in Colombia would likely withstand a potential sovereign downgrade from its current low-tier investment grade, but they will continue to face strong headwinds in 2021 as loan pressures mount.

The South American nation faces risks of a downgrade into so-called junk territory, as greater fiscal challenges and rising debt levels have brought the country under the spotlight of rating agencies. The big three have all placed Colombian debt on negative outlook in 2020, and it is already on the lowest rung of investment grade for both S&P Global Ratings and Fitch, at BBB-.

“It reflects the risk that Colombia delivers low economic growth so that it affects its capacity to consolidate accounts,” Manuel Orozco, a sovereign analyst with S&P Global Ratings, said in an interview, in reference to the sovereign rating and its outlook.

COVID-19-related expenditures contributed to a bloated fiscal deficit of 8.9% of GDP in 2020, with current estimates for this year’s fiscal deficit at 7.6% of GDP. With debt levels hovering above 60% of GDP, economists argue that Colombia could jeopardize its status if it fails to generate new revenue soon.

To that end, President Iván Duque announced he would propose an ambitious tax hike which, according to analysts, has a long road ahead in Congress. Passing the reform, which initially aims to collect 1.5% of GDP, is seen as key to maintain Colombia’s debt ratings.

“Tax reform is absolutely necessary to avoid losing investment grade,” said Munir Jalil, chief economist for the Andean region with BTG Pactual. But it is also “not enough” to guarantee that Colombia will retain the rating, he added.

With presidential elections in Colombia scheduled for May 2022, analysts believe that such a fiscal reform could be either rejected or watered down if it is not sanctioned before the start of political campaigns.

“The best-case scenario is for it to be discussed and approved during the first half of 2021,” Omar Suarez, head of equity with Grupo Aval, told S&P Global Market Intelligence.

Credit pressure is mounting

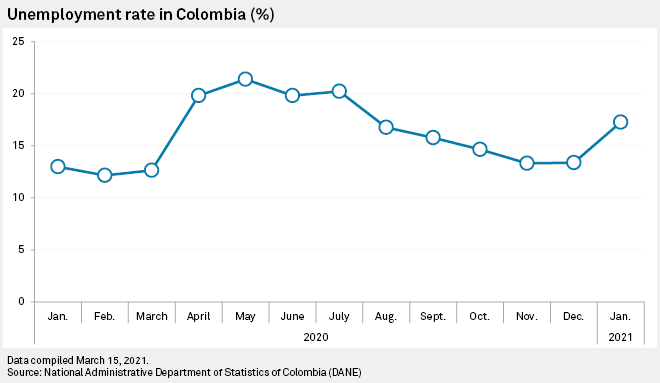

With unemployment spiking to 17.3% in December 2020, concerns on loan assets have risen. Colombian banks are prone to greater asset quality deterioration, as consumer lending strategies pursued prior to the pandemic begin to backfire.

“It just so happened that Colombian banks were in a mini-boom of unsecured consumer loans before the pandemic,” Sebastián Gallego, a bank expert with Credicorp Capital, told Market Intelligence. “That was sheer bad luck.”

As a result, those banks have wound up exposed to a loan segment that, along with loans to small and midsize businesses, is considered to be among the most affected by recurrent lockdowns and restrictions.

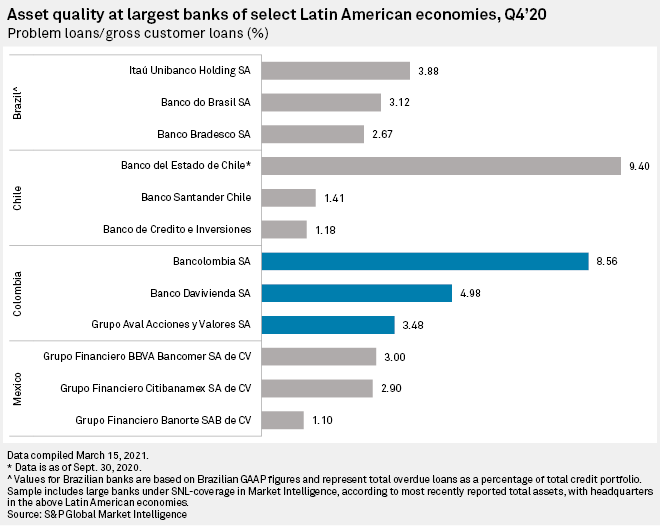

As relief packages come to an end, non-performing loan ratios for top Colombian lenders have begun to rise. Bancolombia SA showed the greatest increase in delinquencies across the largest banks, with the NPL ratio at 8.56% as of the fourth quarter. Banco Davivienda SA follows with 4.98% and Grupo Aval Acciones y Valores SA with 3.48%, Market Intelligence data shows.

“Payment behavior has weakened substantially,” Gallego said. The analyst argued that the average NPL ratio could jump to 7% in the near future. “It will be the highest we have seen in decades,” he warned. However, he underscored that “very robust” liquidity and capitalization levels will keep lenders afloat.

A limited impact on bank funding

While a downgrade at a sovereign level could generate a knock-on effect on several lenders, immediate downside effects would be mostly contained. Experts believe that the increase in the cost of funding for Colombian banks would be limited, as the majority of lenders rely on deposits rather than market access to fund their daily operations.

“There might be an increase in financing costs, but with low rates and so much liquidity among banks, I do not see an impact on that front,” BTG’s Jalil said. Analysts categorically disregard any kind of default event in the near future.

Moreover, domestic banks have taken substantial provisions in order to face future credit losses. The Colombian banking industry held the greatest share of loans under flexibility schemes and payment deferrals. At the height of the crisis, nearly 45% of all banking loans to the private sector were under some form of relief.

That number has been improving since then, but credit risk pressures are still looming.

“Beyond the downgrade (risk), the main challenge for the banking industry continues to be credit risk,” Gallego said. “We are not yet out of the woods in regards to the loan book deterioration cycle that is coming up.”

Tax reform: a double-edged sword?

Although banks would be only partially affected in the short term by a sovereign downgrade, the risks of badly implemented tax reform could be even worse.

As badly as the economy might need reforms, analysts agree that it will be difficult to pass a tax hike without compromising growth. The Colombian economy fell by as much as 6.8% last year and is expected to partially recover in 2021.

“The government has a track record of capacity to raise additional income,” S&P Global Ratings’ Orozco said. “What you want to avoid, however, is that the reform ends up as one of the reasons that kills economic rebound in 2021 and sustained growth in 2022 and 2023,” he added.

“It is a saddle point solution,” BTG’s Jalil said. “The government is aware that it is walking on the edge of the abyss. But the increase in income as of 2022 is so necessary that the tax reform becomes absolutely indispensable.”