A month and a half into the Chilean protests that have spurred senior government resignations and a revamp of the country’s constitution, Chile is on the brink of losing its privileged spot as Latin America’s safest bond investment.

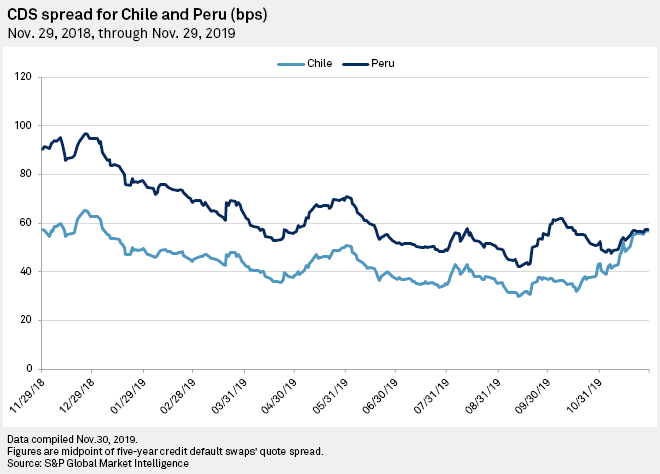

Prices on five-year credit default swaps, a widely used gauge of credit risk, stood at 56.54 basis points as of Nov. 29, spiking by over 50% from 36.87 basis points on Sept. 30. The recent uptick in Chile’s CDS price index has brought its risk metrics to par with that of neighboring Peru, where CDS prices have dropped from a peak of 96.72 basis points last Christmas to its current level of 57.46 basis points.

Although Chile still holds the strongest sovereign debt rating in the region, investors are having second thoughts when it comes to purchasing insurance for its debt. The last time the country’s CDS was not the cheapest was in May 2016, when Uruguay’s insurance price went below Chile’s for a brief period of time.

Chile has been a longstanding icon of financial stability in Latin America, but the lingering effects from the social crisis are leading economists to believe this time might be different, and that the country might no longer be the regional safe haven among LatAm’s most prominent economies.

While the protests originated after the government tried to hike the price of a subway train ticket by 30 pesos, equal to about 4 U.S. cents, they have persisted even after the officials rescinded that decision. The protests since have forced out a number of senior administration officials and have compelled the country to replace its current constitution, which dates back to the nearly two-decadelong dictatorship of Augusto Pinochet in the 20th century.

Faced with plummeting support, President Sebastián Piñera’s center-right government has had to reach a parliament agreement to rewrite the constitution from scratch to address deeply rooted income distribution concerns.

According to Gustavo Rangel, chief LatAm economist with ING, redrafting the constitution could have a material impact on Chile’s economic outlook. “The cost of the protests, both in terms of loss in economic activity and in terms of a fiscal policy price tag, is bound to be high,” he said in an interview. “We just don’t know how high yet.”

Financial markets initially reacted positively to parliament’s agreement to rewrite the constitution, but investors’ hope began to fade as unrest continued. Riots were reported in several spots in the country as recently as late November, with a significant effect on the consumer sector and reported insurance losses that now stand above $2 billion.

Chile’s financial deficit stood at 1.65% by the end of 2018, data collected by S&P Global Market Intelligence shows, one of the region’s lowest. But that might soon change, as newly appointed Finance Minister Ignacio Briones raised the deficit target to 2.9% from 2.0% for 2019, as officials introduce new fiscal measures. A rebuilding program is also underway after weeks of protests.

A report by Moody’s suggests fiscal cost of measures, which include boosting state pension payouts, halting increases in utilities and transportation, as well as expanding government health coverage, will add up to $1.3 billion or 0.4% of GDP in 2020. And that might just be the beginning.

Underlying all this, Chile will face these new budget pressures while dealing with a GDP that has already lost pace, with financial agents under Banco Central de Chile’s market survey now forecasting 1.90% growth for the year, down from 3.6% estimated by the end of 2018.

“Investors are right to be wary,” Quinn Markwith, a Latin America economist with Capital Economics, said. “There is a good degree of uncertainty surrounding just how much the deficit could blow out over this time.”

“Until we get a better idea of what the new constitution will look like in terms of government spending demands, Chile’s debt will likely continue to underperform,” Markwith said.

Yet some hope this might be temporary.

Credit rating agencies have taken a somewhat cautious approach so far, sustaining a stable outlook on the country’s investment-grade debt. Chile holds the highest credit ratings in the region, with an A+ score by S&P Global Ratings, A1 by Moody’s and A by Fitch Ratings.

As of late 2018, public debt in Chile stood at 26.12% of GDP, far lower than its peers’ averages in terms of rating. This could provide some room for attaining social demands without seriously undermining debt repayment capacity, economists say.

“Chile can handle a few years of larger deficits without its debt falling drastically in value,” Markwith said, arguing that expected copper prices rise should “work favorably towards financing its increased spending, and closing the trade imbalance.” Provided the new constitution is “reasonable” and protests “die down,” Chilean debt should perform well over the next years.

But from now on it will likely share the lead, if not eventually lose it to neighboring Peru. Although Lima has seen a fair share of political crisis in recent months, with several impeachment attempts and the dissolution of Congress by President Martin Vizcarra, its economy has nonetheless managed to avoid a full-scale contagion and is expected to sustain economic growth over upcoming years.