Banco Central de la República Argentina is increasingly betting on private fintech initiatives to help foster financial inclusion in the country, though several barriers remain, according to a report obtained by S&P Global Market Intelligence.

The institution noted there is “a strong potential for the emergence of relevant actors” in the digital transformation of banks and in the provision of financial services through digital channels. Fintech initiatives are already engaging users through competitive costs and user-friendly platforms, BCRA specialists wrote in a report responding to Market Intelligence inquiry.

The regulator underscored the importance of growth in virtual wallets as well as the usage of prepaid cards, which can be bought without a traditional bank account. It noted that such cards are seeing “great acceptance” among the underbanked, with over 500,000 cards issued so far.

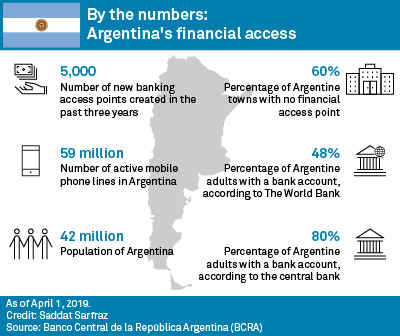

The estimated number of unbanked Argentines vary widely. BCRA claims that 80% of adults have a bank account, while the World Bank’s Findex puts the figure at a much lower 48%.

|

The discrepancy could be due to the vast numbers of individuals who have a bank account but fail to use it regularly, the central bank argued. In Argentina, social benefits and wages must be paid through bank accounts. However, the use of banking resources beyond collecting those and other funds remain limited. Roughly 20% of clients withdraw funds on the first days of the month, leaving their accounts empty through the next paycheck, a manager with a large Argentine private bank, who asked not to be named, said.

According to the central bank, there is a “lack of perception people have of their bank account … and the use that could be made of it.”

In an effort to foster the use of financial services, BCRA has been working to bridge the gap between offline and online transactions. It has adopted the use of so-called QR code payments, based off of square, barcode-like symbols, as well as enabling interoperability between virtual and standard bank accounts. These and other measures, the central bank has argued, have created opportunities for technology companies, fintech firms and online banks.

LatAm e-commerce giant MercadoLibre Inc. has become one of the biggest players here, aggressively deploying a QR network and an increasingly pervasive mobile point-of-sale model across shops in Buenos Aires. The central bank has agreed on a QR standard, but has stopped short of regulating the sector. Unlike Mexico, where the Banco de México is promoting the CoDi payment system, the initiative to expand the reach of financial services in Argentina so far seems to be privately led.

The approval of virtual accounts by the central bank has allowed MercadoLibre to participate in processing welfare program payments. In February, the ANSES Social Security office began testing a pilot program with 300 accounts, in which payments can be collected digitally through MercadoLibre’s e-wallet. If the trials are successful, payrolls could also find their way from traditional bank accounts to online accounts.

According to MercadoLibre executive Osvaldo Giménez, BCRA’s decision to interconnect mobile wallets and bank accounts enhances virtual accounts and puts them on equal terms with traditional bank accounts.

In the wake of these moves, however, BCRA is only now in talks about installing regulations for the fintech sector, something traditional banks have long argued should be in place already. “Banks want to compete, but everybody has to play under the same rules,” one banking source said.

The mobile boom, corresponding agencies

While industry experts have praised the role of smartphones in spurring greater financial inclusion and opening up access routes to reach the unbanked or underbanked population, the mobile boom alone might not be enough.

In its report, BCRA admitted that digital infrastructure is lacking in many parts of the country to support robust digital banking. “Although there are more mobile phone lines than people in Argentina —140 for every 100 inhabitants — barely a third of them have 4G connectivity and there is a high prevalence of prepaid [mobile phone] plans (93%) … all of which might become an obstacle to digital financial inclusion,” the report stated.

As result, the central bank is also working to expand physical financial access points, which are still nonexistent in many parts of the country. According to BCRA figures, 60% of Argentine towns do not have a single physical financial point within their borders.

Here, regulators are relying upon corresponding agencies, a network of merchants that offer financial services within their shops, to help. It was a strategy that proved to be broadly successful in Brazil during the early 2010s. For Argentina, the BCRA called it a “crucial channel to expand access to financial services.”